THE biggest "open secret" when buying properties from developer is that developers offer various freebies and rebates. The rebate given by the developer comes in the form of a deduction against the 10% down payment that the housebuyer is required to make. This rebate fluctuates between 3% and up to a full 10%. By 10% rebate, this means that the housebuyer does not need to pay any down payment and just need to qualify for the balance 90% housing loan. The freebies normally come in the form of free legal fees and / free stamp duty which means that the developer will absorb the legal fees and stamp duty that are required when purchasing a property. Some developers even give freebies in form of household items such as kitchen cabinets, air conditioners, automatic gates system, among other things.

THE biggest "open secret" when buying properties from developer is that developers offer various freebies and rebates. The rebate given by the developer comes in the form of a deduction against the 10% down payment that the housebuyer is required to make. This rebate fluctuates between 3% and up to a full 10%. By 10% rebate, this means that the housebuyer does not need to pay any down payment and just need to qualify for the balance 90% housing loan. The freebies normally come in the form of free legal fees and / free stamp duty which means that the developer will absorb the legal fees and stamp duty that are required when purchasing a property. Some developers even give freebies in form of household items such as kitchen cabinets, air conditioners, automatic gates system, among other things.

Although Bank Negara has instructed that financing by banks is to be based on the net amount after deducting for such freebies and rebates, most financing banks will just turn a "blind eye" and give maximum 90% financing based on the sale and purchase agreement price without deducting for any freebies and rebates.

Many aspiring buyers think that such freebies and rebates make it easier for them to buy their dream home as many housebuyers, especially a first-time housebuyer, may lack the cash to pay for the necessary expenses that the freebies and rebates cover. However, here at the National House Buyers Association (HBA), we are of the opinion that such freebies and rebates do more harm and the Government must put a stop to it.

Everyone is entitled to such freebies and rebates including speculators

It may be true that first-time housebuyers who lack the cash to pay for the necessary payments (such as the 10% down payment, legal fees and stamp duty) will find such freebies and rebates very attractive when they buy their dream home. However, such freebies and rebates are offered to all potential buyers, including speculators, who are out to make a quick gain by flipping the property upon completion or sometimes those even still under construction.

Speculators will always want to accumulate as many properties as possible with the lowest cash outflow. Projects which offer high freebies and rebates will attract speculators and thus depriving genuine buyers the opportunity to own such homes. Upon completion, such speculators will then flip the property and record a handsome gain, their only cost being the progressive interest during the construction period. However, the next housebuyer ends up paying a much higher price in order to buy the property from these speculators.

There is no “free lunch”

Housebuyers must remember that developers are not charitable organisations. Developers are profit-orientated companies and hence, any freebies and rebates given to housebuyers are ultimately factored into the house price.

This means that if the original property price was supposed to be RM700,000 and the developer offers 10% rebate, the developer will then set the selling price at minimum RM777,778 (RM700,000 / 90%). Hence, the selling price of the property has been artificially inflated by RM77,778 but the built quality of the house has not been increased. This artificial increase of RM77,778 puts further strain on future property prices which will be discussed below.

Higher cost and expenses

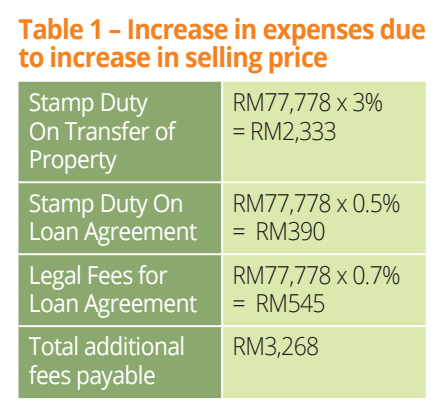

The expenses in buying a property such as legal fees and stamp duties are directly connected to the purchase price of the property. This means that the higher the property price, the higher the legal fees and stamp duty that the buyer must pay.

Let’s just assume that in the example above, the developer wanted to launch a project at RM700,000 and is offering a rebate of 10%. The developer will then price the property at RM777,778 (being RM700,0000 / 90%). The additional cost that the house buyer will need to pay is as follows:

Higher loan interest

As explained above, the cost of all freebies and rebates will be factored into the house price and what it means in a nutshell is that housebuyers just take a higher loan and pay it over the tenure of the said housing loan.

In our example above, due to the house price being increased from an earlier target of RM700,000 where the buyer would have to pay 10% down payment and take a RM630,000 loan, the house buyer now has to take a RM700,000 housing loan (based on the revised selling price of RM777,778 * 90% financing) instead of RM630,000 if the property was sold without rebates.

Based on an effective interest rate of say 4.40%, the borrower has to pay the following incremental interest:

Will lead to higher house prices in the secondary market

The prices of new properties sold by developers or also known as primary property market and existing completed properties that are owned by the general public or also known as secondary property market are inter-linked.

When there is an increase in prices of primary properties, existing owners will try to increase the asking prices of the secondary market. In addition, developers will always conduct a survey on the prices of the secondary market before launching their new projects and will always set a premium to the prices offered by the secondary market. Developers will also launch their future projects at a premium compared to the previous launch.

When the price of the primary project has been artificially increased by RM77,778 in our current example, the prices of the secondary market will try to match this increase by also increasing their asking prices when they want to sell their homes. This will then result in increase in prices of the surrounding secondary market making it more difficult for future buyers to own such properties.

When the developer wants to launch their next project, the selling price will then have to be set at a premium to RM777,778 and not RM700,000. This will further put a strain on prices of secondary market to follow suit.

Property prices also have a spill over effect. The increase in property prices due to rebates above can spill over to surrounding locations. Hence, property prices increase in say, Kepong, can push up prices of properties in Cheras and eventually over time even push up properly prices as far as Kajang and Semenyih.

As a result, properly prices in many urban and even sub-urban areas have become seriously unaffordable to severely unaffordable as highlighted by Khazanah Research Institute. HBA has warned the Government that unless strong action is taken to address this issue, an entire "homeless generation" could emerge that is unable to buy their own homes and this can bring about various social problems.

Is there a solution?

It is clear that freebies and rebates do more harm than good and this practice must be stopped immediately. Banks must heed Bank Negara's directive that financing is based on the net amount after deducting for all freebies and rebates if developers are unwilling to stop this practice.

Banks can consider giving 100% financing for all first-time housebuyers (not that we encourage them to do so) for all affordable properties that cost below RM300,000 and subject to the housebuyers meeting the credit criteria of the individual lending banks. However, there should be a lock-in period of 10 years where the house buyers are prohibited from selling such properties to discourage speculators from abusing such Affordable Properties or relaxed lending conditions.

Housebuyers must also start saving up for their dream home from an early age. Housebuyers must realise that they must have at least 15% of the purchase price of the property in cash to cover the 10% down payment and other ancillary expenses. This means that all aspiring buyers must set aside a portion of their salaries to buy a property immediately when they start working and forgo certain luxuries such as that RM10 coffee or to buy the latest electronic gadgets or even to own a better car.

Although it is possible to use the Employees Provident Fund (EPF) savings to cover the 10% down payment, aspiring housebuyers should try to save up as much as possible without resorting to using the EPF savings which is actually meant for retirement.